Riding Out the Storm: What a Century of Recessions Can Teach Small Businesses

Every few years, the word “recession” starts making headlines and stirring anxiety. For a small business owner or startup founder, talk of an economic downturn can feel like storm clouds gathering on the horizon. Is another downturn coming? When it does, what will it mean for your business? While recessions are certainly disruptive, they are also a recurring part of economic life – the U.S. has experienced dozens of recessions since its founding, including 14 official recessions since the Great Depression, averaging one every 6–7 years. Rather than panic, business owners can benefit from taking the long view. By looking at how past U.S. recessions began, what early warning signs were visible, and how those downturns played out globally and for small businesses, we can glean insights to navigate whatever comes next. This blog post will blend historical analysis with a practical, conversational tone to help demystify recessions – showing not only the threats they pose, but also the opportunities they can present.

We’ll start by examining the early signs of recession and notable patterns across the 20th and 21st centuries. Next, we’ll explore how U.S. recessions have impacted the global economy, turning local troubles into worldwide challenges. Then we’ll zero in on small businesses – how recessions have hit Main Street and how some businesses managed not just to survive but to thrive in hard times. Finally, we’ll offer strategic reflections to help anticipate future recessions and prepare with foresight, so you can face the next storm with resilience. Let’s dive into the lessons of history to better weather the economy of tomorrow.

Early Warning Signs: How Recessions Begin

How can you tell a recession might be coming? Economists have long searched for reliable warning indicators that the economic party is about to end. No one has a crystal ball, but history has revealed some common patterns that precede downturns. One of the most famous signals is the inverted yield curve – a wonky term for when short-term interest rates exceed long-term interest rates. In normal times, lenders demand higher interest for long-term loans than short-term ones. But if investors become pessimistic about the long run, long-term yields drop below short-term yields, inverting the curve. This indicator has an uncanny track record: . In other words, when you see the yield curve flip upside-down, it’s often a harbinger of rough economic weather ahead. (Indeed, an inversion in 2022 raised concerns about 2023–24.)

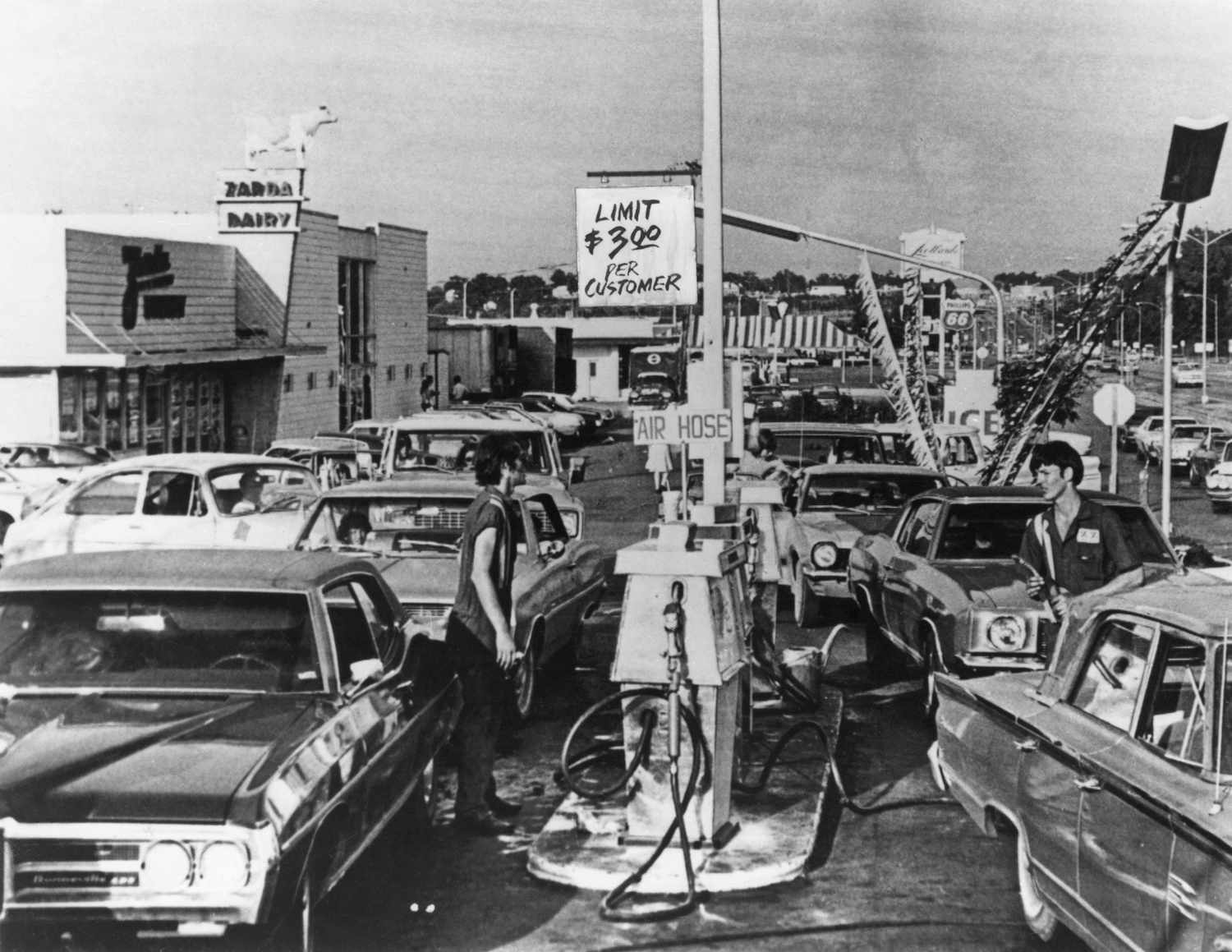

Another classic warning sign is rising interest rates and tightening credit conditions. Typically, late in an economic boom, the Federal Reserve (and other central banks) start raising rates to pump the brakes on inflation or speculative excess. History shows that as policymakers try to cool an overheating economy. For example, in the late 1920s the Fed quietly tightened monetary policy, and in the 1970s and early 1980s interest rates were pushed to painfully high levels to combat inflation – moves that ultimately tipped the economy into recession. Surging prices of key commodities can flash warnings too: oil shocks in particular have foreshadowed recessions. A steep jump in oil prices acts like a tax on consumers and businesses, often shrinking demand. The oil embargo of 1973 is a dramatic case – crude prices more than doubled within months, which helped send the U.S. (and much of the world) into a deep slump by 1974.

History also teaches us to watch out for asset bubbles and bursts of “irrational exuberance.” A roaring stock market or housing market can signal that investors are overly optimistic, and that a painful correction may loom. In the summer of 1929, for instance, the stock market was red-hot after a decade of rapid gains. Many observers realized the pace of stock price increases was unsustainable. A few prescient voices, like economist Roger Babson, even warned publicly that “sooner or later a crash is coming” – and were largely mocked or ignored. Famously, only days before the Wall Street Crash of October 1929, Yale economist Irving Fisher blithely declared that stocks had reached “a permanently high plateau”. We know how that turned out. In hindsight, underlying cracks were forming even as 1929’s market hit record highs – industrial production had begun to decline and unemployment was creeping up, leaving stock prices disconnected from economic reality. Similarly, before the dot-com bust in 2000, tech stocks soared to absurd valuations despite many internet startups having no profits. And before the 2008 financial crisis, U.S. home prices and subprime mortgage debt skyrocketed beyond sustainable levels. When those bubbles burst, recession followed.

None of these signs alone guarantees a recession – the economy is complex, and sometimes false alarms happen. But when multiple warning signs start flashing together (for example, an inverted yield curve rapidly rising interest rates an asset market that feels like a bubble), history suggests it’s wise to buckle up. As a small business owner, keeping an eye on big-picture indicators like these can provide valuable lead time. The goal is not to panic at every flicker of bad news, but to stay informed about the economic context in which your business operates. Recessions rarely strike completely without warning; by recognizing the patterns in advance, you can start preparing before the storm hits.

A Historical Tour: U.S. Recessions Across the Decades

To better understand recessions, let’s take a journey through some of the most significant U.S. downturns of the past century. Each recession has its own story and causes, but they also share some common threads. Seeing how they unfolded can deepen our perspective on what to expect when the next one comes.

The Great Depression (1929–1933)

No discussion of recessions can begin anywhere else. The Great Depression remains the worst economic contraction in U.S. history, and a kind of cautionary tale of how bad things can get. It began with the stock market crash of October 1929, which wiped out billions in wealth virtually overnight. But the crash was more symptom than root cause – the U.S. economy in the late 1920s had underlying weaknesses (farmers in debt, industrial overcapacity, shaky banks) masked by the stock euphoria. Once the bubble burst, panic set in. From 1929 to 1933, U.S. GDP fell by roughly 27% and unemployment spiked to about 25%. Thousands of banks failed, wiping out savings. Deflation (falling prices) made debts harder to pay. It was an economic free-fall, and it did not hit the U.S. alone – it became a global depression (as we’ll explore further below). Images of the era, like lines of unemployed men at soup kitchens, capture the human toll. After 1933, the economy slowly began to recover (helped by New Deal policies), but the Depression’s shadow was long. One lesson it taught painfully well: allowing the financial system to collapse can turn a bad recession into a catastrophe. This led to reforms like federal deposit insurance and stricter bank regulation in the 1930s, aimed at preventing a repeat. Indeed, since World War II, U.S. recessions have thankfully been milder than the Great Depression, with no downturn coming close to the same depth until 2020’s pandemic crash.

Post-WWII Booms and Busts

In the prosperous decades after World War II, the U.S. experienced a series of shorter recessions (in 1949, 1953, 1958, 1960, etc.) typically followed by strong recoveries. These recessions often coincided with the Fed raising interest rates to cool inflation or with the winding down of wartime spending. A notable one was the Recession of 1957–58, when a combination of high interest rates and a slump in manufacturing led to a quick downturn. Unemployment hit 7.5%, but the recession lasted under a year. Generally, in the post-WWII era the economic cycle became more moderate: recessions from 1945 through 2001 lasted about 10 months on average, versus 18 months in the interwar period. Economists call this post-war stability the “Great Moderation,” attributing it to better policy (like smarter Fed management and automatic government stabilizers such as unemployment insurance) and a more diversified economy. Of course, “moderate” is relative – to those who lived through layoffs and factory closures in say, 1958 or 1982, the pain was still very real. But compared to 1930s-scale devastation, recessions became milder overall.

Stagflation and the Double-Dip (1970s–early 1980s)

By the late 1960s, the U.S. economy hit a new kind of turbulence. The 1973–75 recession was triggered in large part by the OPEC oil embargo. In October 1973, Middle East tensions led oil-producing nations to cut off exports to the U.S., and the price of oil quadrupled within months. Suddenly, gasoline was expensive and in short supply, hitting both consumers and businesses hard. At the same time, inflation was already rising. The result was “stagflation” – stagnant economic output coupled with high inflation – a nasty combination. The 1973–75 downturn lasted roughly 16 months, with GDP contracting and unemployment reaching about 9%. It was one of the lengthiest and most painful recessions of the post-war period. Unfortunately, relief was short-lived. After a brief recovery, a second recession struck in 1980–1982, creating what some called a “double-dip.” The proximate cause was the Federal Reserve’s aggressive campaign to finally break the back of double-digit inflation. Under Chairman Paul Volcker, the Fed hiked interest rates to unprecedented heights (the federal funds rate hit ~19% in 1981) – a shock therapy for the economy. This succeeded in taming inflation, but at the price of back-to-back recessions. The unemployment rate soared above 10% in 1982, the highest since the Depression up to that point. Businesses, especially interest-sensitive ones like housing and manufacturing, were pounded by the high cost of credit. By late 1982, inflation was finally under control and the Fed eased up, allowing a strong recovery to begin. The lesson from this era? Recessions can be caused not only by “bubbles bursting” but also by policy choices: the cure for runaway inflation was deliberately induced economic pain. For small businesses, the early ‘80s were extremely challenging – but once inflation was purged, the stage was set for the long, stable expansion of the 1980s and 1990s.

The Dot-Com Bust (2001)

Fast forward to the turn of the 21st century. The U.S. enjoyed a booming economy through the 1990s, but by 2000 a speculative fever had built up around internet and technology stocks – the “dot-com bubble.” In early 2000, that bubble burst spectacularly. The NASDAQ stock index (packed with tech companies) plunged by 75% from 2000 to 2002, wiping out trillions in market value. Surprisingly, the broader U.S. economy initially continued chugging along despite the stock crash – many Americans outside of Wall Street didn’t feel the effects right away. It wasn’t until the shock of the 9/11 terrorist attacks in September 2001 that the economy truly faltered. The combination of the investment downturn and the post-9/11 disruption led to a recession in 2001. Thankfully it was relatively brief and shallow as recessions go: U.S. GDP fell only about 0.3% overall, and unemployment peaked around 5.5%. In fact, many Americans didn’t even realize a recession had happened – it officially lasted just 8 months (March to November 2001). One reason it stayed mild was that other parts of the economy (like housing and consumer spending) held up well, aided by low interest rates at the time. The dot-com crash taught investors a lesson about “irrational exuberance,” but the episode showed that not every market crash guarantees an economic collapse. Still, it was a wake-up call about how overinvestment in unproven ventures can create vulnerabilities that eventually impact the real economy.

The Great Recession (2007–2009)

If you’re a business owner today, the recession you probably remember best is the Great Recession of 2007–09. This was the most severe downturn in the U.S. since the 1930s – a sobering reminder that financial crises can still happen in the modern era. The Great Recession was triggered by a collapse in the U.S. housing market. Throughout the early 2000s, low interest rates and easy credit fueled a housing boom and a surge in subprime mortgage lending (loans to borrowers with shaky credit). Home prices soared and financial institutions bundled mortgages into complex securities. It was, in effect, a housing bubble built on a house of cards. When home prices started falling in 2006–07, the whole edifice began to crumble. By 2008, major Wall Street firms that had gorged on mortgage-backed securities were imploding – Bear Stearns collapsed, and Lehman Brothers went bankrupt in September 2008, nearly bringing down the global financial system. The result was a global financial meltdown with the U.S. at the epicenter. Credit markets froze and stock markets worldwide plunged. The U.S. economy went into a tailspin: GDP contracted by 4.3% and unemployment climbed to 10%. This “Great Recession” lasted 18 months (Dec 2007 to June 2009) and was felt in virtually every sector. What made it especially frightening was the contagion effect – this was not just a normal business cycle slowdown, but a crisis of confidence in the financial system. The federal government intervened with unprecedented rescue measures (over $1.5 trillion in stimulus and bailouts) to stabilize banks, automotive companies, and more. Those actions eventually stopped the bleeding and set the stage for recovery. For small businesses, the 2008–09 period was extremely tough: consumers cut spending, banks drastically pulled back lending, and many entrepreneurs saw years of growth wiped out. Yet, the upheaval also cleared the way for a new era of innovation in the 2010s (more on that soon).

The COVID-19 Recession (2020)

Lastly, we come to a very recent downturn – the flash recession caused by the COVID-19 pandemic. This episode was highly unusual. In early 2020, as the coronavirus spread globally, governments imposed lockdowns and travel halts for public health reasons. Economic activity came to an abrupt standstill in many industries. The U.S. (and virtually every advanced economy) entered a sudden recession in March 2020. The numbers were astonishing: over 20 million U.S. jobs vanished in a single month, and GDP contracted at an annualized rate of 31% in the second quarter of 2020 – an economic plunge even sharper than the worst quarter of the Great Depression. However, this downturn was very short-lived. By summer 2020, massive government relief spending (nearly $6 trillion in the U.S.) and emergency Fed actions propped up the economy. As lockdowns eased, growth bounced back rapidly. The recession officially lasted only two months (February–April 2020), the shortest on record, although the recovery from the pandemic had uneven effects on different sectors. The COVID recession showed how an external shock (a virus) can instantly throw a modern economy into deep freeze – but it also demonstrated the power of swift policy response to create a bridge to recovery. Small businesses were hit especially hard by the pandemic, with many forced to close temporarily or adapt on the fly, but stimulus programs like PPP loans helped some stay afloat. In the end, while incredibly intense, the COVID recession was brief. It underscores that not all recessions follow the slow-building pattern of a financial crisis; some strike out of the blue and then dissipate quickly.

As we see from this historical tour, U.S. recessions have varied widely in cause and severity. Some were triggered by financial excess (1929, 2008), others by policy tightening or external shocks (1981’s rate hikes, 1973’s oil embargo, 2020’s pandemic). Recessions can be short and mild or long and grinding. Yet a few themes emerge. Often, a boom precedes the bust – whether it’s a boom in stocks, housing, credit, or something else – and imbalances build up that eventually need correcting. Also, government responses matter: smart intervention can shorten a recession, while policy mistakes can worsen it. And crucially for business owners, every recession does end eventually, and the economy moves into recovery and expansion again. Keeping this historical perspective in mind can be comforting in tough times. As one era’s downturn passes, a new expansion – and new opportunities – inevitably arise.

Global Ripples: U.S. Recessions and the World Economy

Because the United States is the world’s largest economy, when America sneezes, the world often catches a cold. U.S. recessions have a way of spreading far beyond U.S. borders, especially in our increasingly interconnected global economy. A downturn that starts on Wall Street or Main Street can quickly ricochet through trade links, financial markets, and investor confidence worldwide. History provides plenty of examples of these global ripple effects.

The Great Depression of the 1930s is the classic case. What began as a financial crash in New York soon became a worldwide economic collapse. As U.S. demand for foreign goods plummeted and American banks called in overseas loans, other countries were dragged down. European economies, many still weakened from World War I, were hit extremely hard – for instance, Germany’s industrial output fell by nearly half by 1932, and Britain, France, and others suffered severe contractions. International trade entered a tailspin. In a misguided attempt to protect their own industries, the U.S. enacted the Smoot-Hawley Tariff in 1930, hiking tariffs on imports. Many countries retaliated with their own tariffs, which only choked off trade further. Worldwide, global trade collapsed by roughly 65% in the early 1930s. Without foreign markets or capital, economies from Latin America to Asia shrank; commodity prices for products like coffee, cotton, and rubber plunged, hurting exporting nations. The Great Depression thus became a truly global depression. It also contributed to political upheaval around the world, as extreme economic distress fueled instability (one notable example: economic woes were a factor in the rise of militarist regimes in Europe and Asia in the 1930s). The painful lesson learned was that economic isolationism and beggar-thy-neighbor policies (like competitive tariffs) can deepen a global downturn. In later decades, world leaders strove to cooperate more during crises – for instance, creating institutions like the International Monetary Fund to coordinate responses.

In the post-war era, many major U.S. recessions were mirrored in other advanced economies. The oil shock of 1973 didn’t just hurt the U.S.; it caused stagflation in Europe and Japan as well. In the early 1980s, the U.S. Fed’s interest rate hikes not only tamed U.S. inflation but also sent shockwaves through developing countries. Countries in Latin America had borrowed heavily in the 1970s when money was cheap; when U.S. rates skyrocketed, their debt payments became unmanageable, leading to the 1980s “Debt Crisis” across Latin America. Thus, a U.S. policy decision (raising rates) played a role in a wave of global sovereign debt defaults. More broadly, since the 1970s the world has seen several episodes of “synchronized recession,” where multiple regions contract together. Most of these episodes have coincided with U.S. recessions. For example, the early 1980s recession was felt across many Western economies at once, and the early 1990s saw the U.S., U.K., and parts of Europe in recession simultaneously after the Cold War boom faded. The U.S. economy’s sheer size and its financial ties (through banks, investors, and supply chains) act as a conduit: when the U.S. slows, its trading partners often lose export sales and its financial tremors can unsettle markets abroad. In today’s era of globalized commerce, a small business in Asia or Europe might find fewer American customers or tighter credit when the U.S. hits a downturn.

The Great Recession of 2007–09 is a vivid contemporary example of a U.S.-led global crisis. The meltdown in U.S. housing and banking triggered a global financial crisis. European banks had also invested in U.S. mortgage securities, so they suffered huge losses; major institutions in the UK, Germany, France, and beyond needed bailouts. Global stock markets fell in tandem. Many countries, not just the U.S., entered recession by 2008. In fact, the period 2008–2009 saw the first outright decline in global GDP since World War II. U.S. recessions had generally been getting milder over time, but episode reversed that trend – it was among the deepest worldwide downturns of the postwar era. For instance, Europe’s economy contracted sharply in 2009, and some nations (like Greece) went on to experience a debt crisis partly due to the damage of the Great Recession. Emerging markets from Eastern Europe to Latin America also took hits as foreign investment dried up. In short, 2008 proved that a financial crisis in the U.S. can rapidly escalate into a global recession, given how tightly linked capital markets are. On the positive side, it also spurred coordinated international action: the U.S., EU, China, and others all launched stimulus measures, and central banks around the world cut rates in unison to fight the downturn.

Even the 2020 COVID-19 recession, while caused by a global pandemic rather than a U.S.-specific issue, demonstrated economic synchronization. Virtually every country went into recession simultaneously in 2020 when the virus spread. The U.S. was part of that, of course – its steep drop in imports and abroad travel hurt economies reliant on American tourists and buyers. But unlike in 2008, the U.S. wasn’t the singular cause; it was one of many victims of a common shock. Still, the pandemic showed how globally intertwined we are: supply chain disruptions in one region could idle factories in another, and recovery in one country was linked to health outcomes in others.

For small businesses, the global dimension of recessions might seem abstract – after all, your primary concern is your local market, your customers, and your community. But it’s worth remembering that we operate in a globally connected environment. A U.S. recession that weakens the dollar or lowers domestic interest rates might, for example, make imported goods cheaper (a benefit to some businesses) or reduce foreign tourist traffic (a drawback to others). Conversely, a downturn abroad can boomerang back – if key overseas suppliers or buyers face trouble, it can impact your supply chain or sales. The main takeaway is that no economy is an island. By staying attuned to international as well as national trends, business owners can better understand the full context of a recession’s impact. In modern times, U.S. recessions “have increasingly affected economies on a worldwide scale, especially as countries’ economies become more intertwined”. The silver lining is that globally coordinated responses can also help speed recovery. As we saw in 2009 and 2020, nations working together (through joint rate cuts, stimulus, etc.) can put a floor under a global slump.

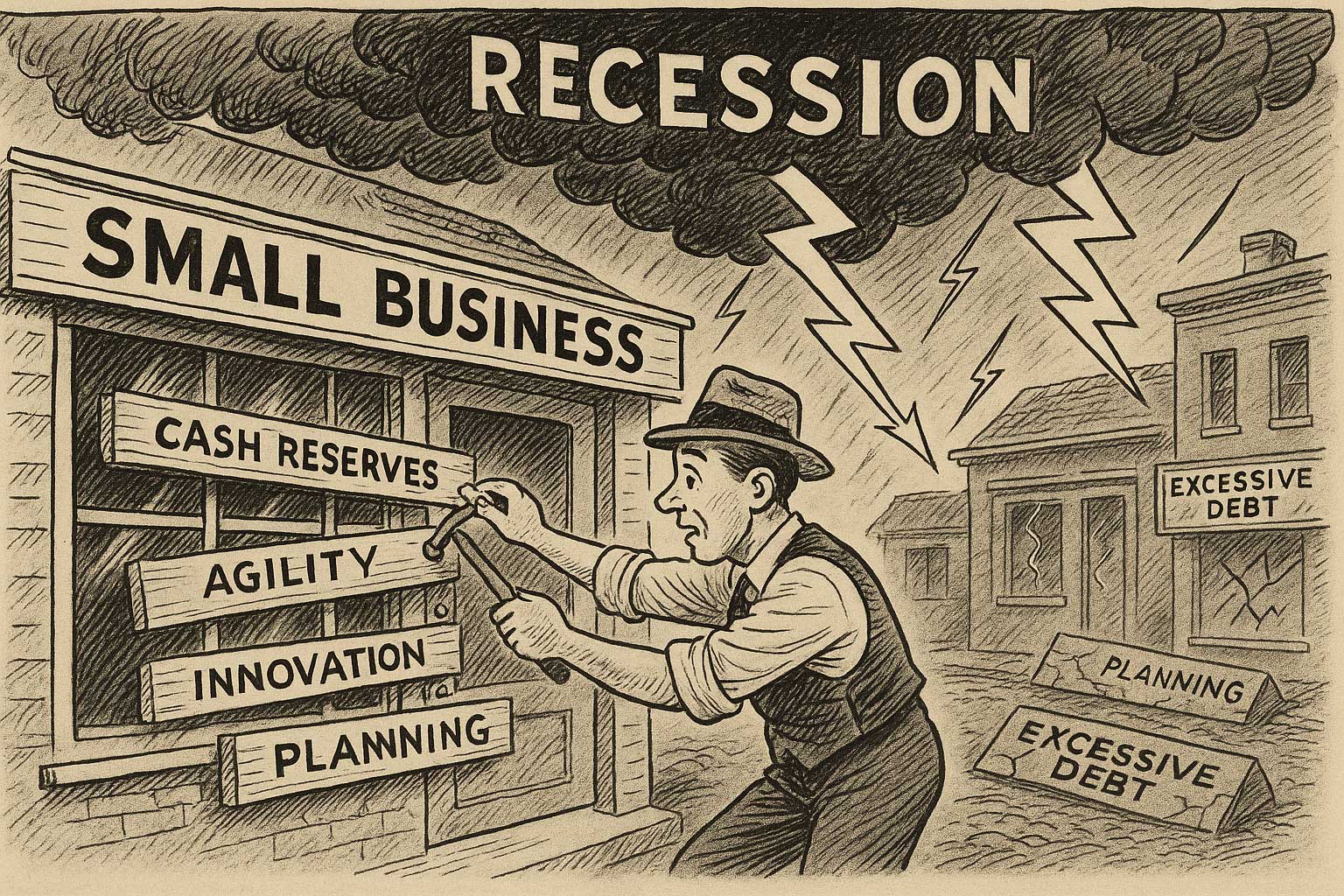

Main Street Realities: Small Businesses in Recession (Threats and Opportunities)

When recession hits, it often hits small businesses the hardest. By nature, small and mid-sized businesses lack the deep financial buffers, diversified product lines, and access to capital that large corporations enjoy. A big company might weather a few bad quarters by tapping bond markets or shifting operations overseas – options that your neighborhood restaurant, local retailer, or startup simply doesn’t have. Indeed, small firms “tend to fare worse than larger ones in a recession” because they have less ability to withstand a sharp drop in revenue amid mounting uncertainty. Let’s break down what challenges a recession brings to Main Street, and then explore how some small businesses manage not only to survive but even find opportunity in these tough times.

The Challenges: In a downturn, the most immediate problem for a small business is typically falling demand. Customers tighten their belts, meaning fewer sales at the register. For many businesses, even a modest dip in revenue can upset the delicate balance of costs and income. Unlike giant firms, small businesses often operate on thin margins – they don’t have huge cash cushions. As one analysis put it, small businesses have a smaller margin of error when the economy sours. If sales drop, that cash flow you rely on to pay rent, suppliers, and employees can dry up fast.

Another major challenge is access to credit and capital. Banks and lenders become risk-averse during recessions. A small company without significant assets or a long track record may find it difficult to get a loan or line of credit when it needs it most. According to the Federal Reserve Bank of New York, in the wake of the 2008 recession, many banks cited “poor sales and economic uncertainty” as reasons for tightening credit to small firms. In practical terms, that means if you run a small business and try to borrow to cover a shortfall, you might be turned away precisely because the economy is in bad shape – a frustrating catch-22. Smaller enterprises also typically lack the ability to issue stock or bonds to raise funds, unlike large corporations. So they rely on personal savings, credit cards, or loans secured on personal assets, which may be in short supply during hard times. All of this can lead to liquidity crunches. If bills pile up and credit can’t be obtained, insolvency looms. Unfortunately, it’s common to see spikes in small business closures and bankruptcies during prolonged recessions.

Recessions also force tough operational decisions. Costs often need to be cut quickly to match the new reality of lower income. This can mean laying off valued employees (or freezing hiring), reducing inventory, cutting marketing budgets – all painful measures that can hurt morale and future growth potential. For example, during the 2020 COVID shock, thousands of small retailers and restaurants had to furlough staff or drastically scale back operations overnight. Even in a milder recession, a small business owner might go from thinking about expansion to suddenly worrying about how to pay this month’s bills. The stress level can be intense, as many entrepreneurs pour their hearts into their businesses and feel a personal responsibility for their employees’ livelihoods.

In short, a recession brings a cascade of threats to small companies: slumping sales, tighter credit, slower customer payments (as clients themselves struggle), and pressure to cut costs. It’s no surprise that many smaller firms don’t make it through a severe downturn. For those that do, the scars may include depleted savings, debt burdens, or lost talent.

The Opportunities: Yet, it’s not all doom and gloom. History shows that recessions, while destructive, can also clear the field for new growth. There’s a concept in economics known as popularized by economist Joseph Schumpeter. The basic idea is that downturns , “clearing the ground for a fresh burst of innovation.” As one Federal Reserve summary of Schumpeter’s theory describes. In plain terms, when weaker businesses fail, surviving companies can seize a larger market share, and new innovative players often emerge to fill unmet needs.

For small business owners with the grit and skill to outlast the storm, a recession can actually become an opportunity to come out stronger relative to competitors. The most capable survivors may find that when the dust settles, some of their rivals have disappeared, leaving a larger customer base up for grabs. As Investopedia notes. We saw this after 2008: many small firms that survived the Great Recession found less competition in certain markets, and when consumers returned, those survivors grew rapidly.

Recessions can also unleash entrepreneurial creativity and innovation. When “business as usual” breaks down, it creates openings for new solutions. Interestingly, a number of hugely successful companies have been born recessions – often started by founders who spotted an opportunity amid the chaos or who simply had nothing to lose after losing jobs elsewhere. A few famous examples: Microsoft was founded in 1975, in the middle of the 1973–75 recession, by two young programmers (Bill Gates and Paul Allen) who believed software was the future. Airbnb launched in 2008 when its founders rented out air mattresses in their apartment to travelers during the Great Recession – today it’s a global hospitality giant. Uber was founded in early 2009 in San Francisco at the recession’s bottom, when taxi service was lacking and laid-off tech workers were looking for gigs. There are many such stories. The takeaway isn’t that recessions are “good” – clearly they cause a lot of pain. But constraints can breed resourcefulness. If a small business can identify how customer behaviors are changing in a recession (e.g. demand for cheaper alternatives, or new needs created by the situation), it can pivot more nimbly than big corporations. We saw countless small businesses do this during the COVID-19 recession: restaurants switched to take-out and delivery models, distilleries started making hand sanitizer when there was a shortage, gyms moved to online classes, and so on. Some of those innovations created new revenue streams that lasted even after the recession ended.

Another potential advantage for small businesses in a downturn is the ability to build stronger customer loyalty and community ties. In hard times, consumers often turn to people and businesses they trust. A local business that demonstrates empathy – say, by offering flexible payment plans, or supporting community relief efforts – might deepen its relationship with customers, who remember that goodwill later. Small businesses are rooted in communities, and that local connection can be a lifeline. There’s also an opportunity for savvy small businesses to hire talent that may become available during layoffs from larger companies. When big firms cut staff, the available pool of skilled employees grows. A small company that is in a position to hire (or even just contract freelancers) might pick up great people it otherwise couldn’t afford, setting the stage for future growth.

In essence, recessions force businesses to adapt. Those that adapt well can emerge more efficient, more innovative, and with a larger market presence. Of course, none of this minimizes the very real risks. Many small enterprises will understandably play defense in a recession – cutting costs and focusing on core customers to survive. But keeping an eye out for the strategic openings that downturns present is important. Whether it’s acquiring a competitor’s assets on the cheap, targeting a neglected customer segment, or launching that creative idea you’ve been mulling (because suddenly the old rules don’t apply), a recession can be a time to execute bold moves that position you ahead of the pack when growth returns.

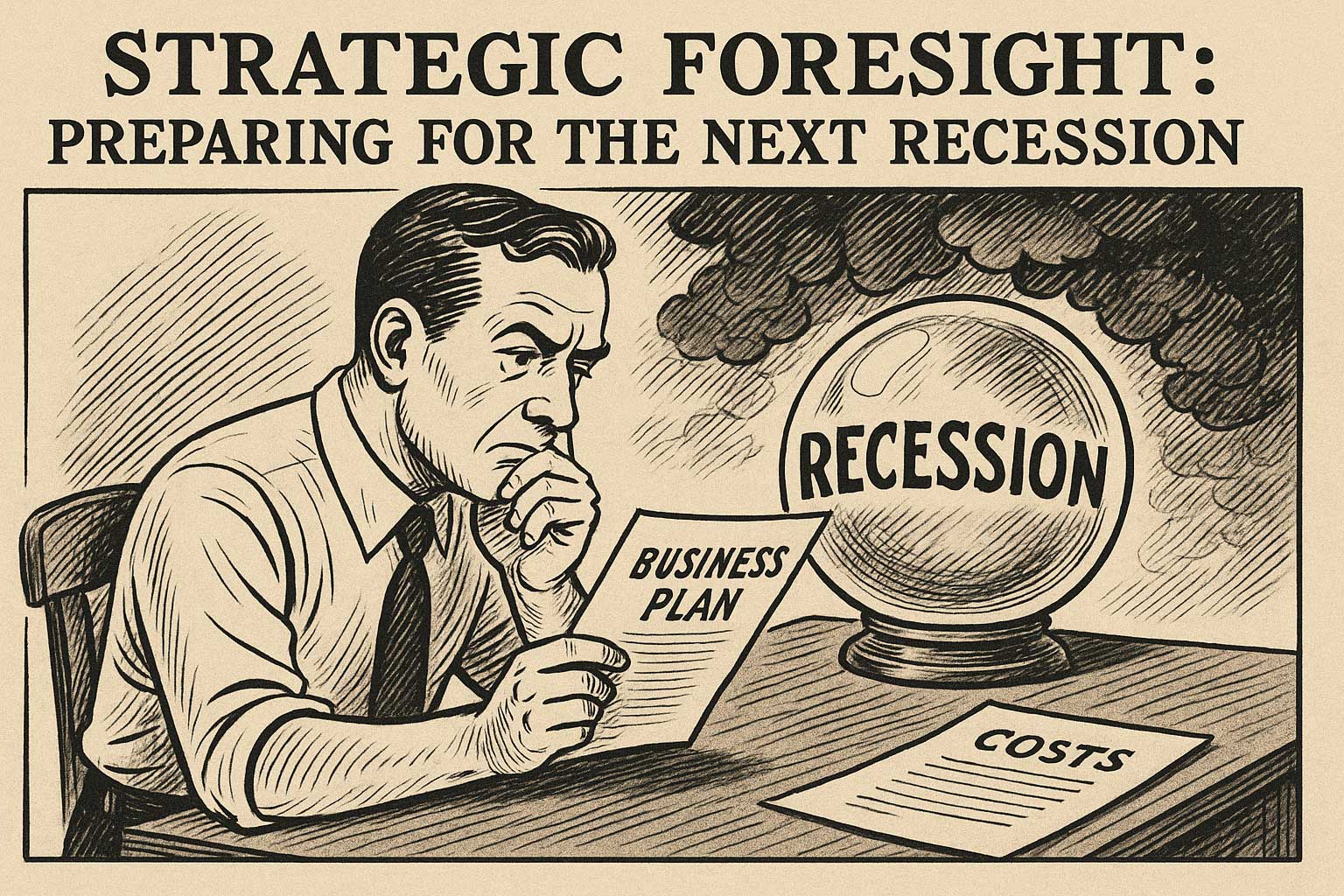

Strategic Foresight: Preparing for the Next Recession

Economic downturns are inevitable – we can’t wish them away. But as a small business or startup, you don’t have to be at the mercy of the cycle. While you can’t control macroeconomic forces, you control how you prepare and respond. In this final section, let’s discuss how you can apply the insights from history to anticipate and navigate future recessions with strategic foresight. Think of it as assembling your business’s storm kit in advance, and charting out how you’ll ride out the rough seas.

1. Stay Informed and Alert to Economic Signals.

First, cultivate a habit of tracking economic indicators that are especially relevant to your business. You don’t need to be an economist, but keeping an ear out for key signals – like interest rate trends, consumer confidence, and yes, even the yield curve – can give you a timely heads-up. As we covered earlier, an inverted yield curve or rapid rate hikes can be red flags that a slowdown is likely. If you know a bit in advance, you can start planning (for instance, holding off on that risky expansion, or securing financing before credit tightens). Similarly, pay attention to your own industry’s signs of softness – maybe you notice customers taking longer to pay or sales inquiries dropping off. Those on-the-ground signals are just as important as the headline news. Essentially, tune your radar: the goal is to recognize the winds of change early, rather than being caught off-guard.

2. Fortify Your Finances.

When times are good, it’s easy to get complacent, but that’s exactly when to strengthen your balance sheet. History shows that companies with lean operations and healthy finances face recessions with a huge advantage. In practical terms, this means building cash reserves and managing debt wisely. Cash is king in a downturn – it gives you flexibility to cover expenses if revenue dips, and even to invest in opportunities when others can’t. Many seasoned entrepreneurs aim to have a cash buffer that can cover at least a few months of operating costs. Reducing high-interest debt before a recession hits is also prudent, as credit can become more expensive or unavailable later. A diversified revenue stream can help as well. If all your income comes from one big client or one product, your business is more vulnerable. By diversifying – perhaps offering a mix of products, serving a range of customer types, or expanding to online sales if you mostly rely on foot traffic – you spread out the risk. In summary, shore up your liquidity and avoid overextension during the boom times so that you enter the bust as financially fit as possible. It’s the business equivalent of reinforcing your house before the hurricane.

3. Plan for Different Scenarios.

Uncertainty is a given in recessions. You may not know exactly how hard you’ll be hit or for how long. That’s why scenario planning is a valuable exercise. Consider making a simple contingency plan for a mild recession vs. a severe one. Ask questions like: “If our sales fell 20%, what costs would we cut or what alternate income could we tap?” “Which expenses are truly essential and which can be trimmed?” Identify triggers that would prompt certain actions (for example, if monthly revenue falls below X, then pause new hiring or renegotiate the lease). By sketching these out in advance, you won’t be scrambling to make decisions under duress – you’ll have a rough roadmap. Importantly, plan not just for defense but also for potential offensive moves. What investments would you still want to make even in a downturn (e.g. marketing to retain key customers, or R&D for a product launch timed with the recovery)? Research from Harvard Business Review has shown that companies which balance cost-cutting with selective investment during recessions tend to outperform those that only cut or only invest blindly. So, chart out what a balanced strategy looks like for you. Think of it as preparing for a rainy day while also being ready to plant seeds for the future.

4. Maintain Agility and Customer Focus.

Small businesses actually have a big advantage over larger ones in one respect: agility. You can pivot faster and personalize more. In a recession, be ready to adapt your business model or offerings to meet changing customer needs. This might mean adjusting price points (offering smaller, more affordable options or promotions to retain price-sensitive customers), or emphasizing your value in terms of cost savings. For example, if you sell a product that helps other businesses save money or operate more efficiently, highlight that benefit – in downturns, clients are looking to cut costs. It could also mean targeting new customer segments that emerge. The key is to listen closely to your customers’ pain points and be willing to tweak your approach. Additionally, recessions are a crucial time to double down on customer service and relationships. People might be cutting back, but they will stay loyal to businesses that treat them well and provide genuine value. Communicate proactively with your customers; if you’re a B2B company and anticipate any supply delays or changes, let your clients know early and work with them on solutions. This builds trust. Loyal customers can become a stable source of revenue even when new sales are hard to come by. Moreover, as competitors falter, you might capture their disenchanted customers by offering a helping hand. In essence, be the business that customers rely on when times are tough, and they’ll likely reward you with long-term loyalty.

5. Keep Your Team Motivated and Lean.

Your employees are a critical asset in navigating a recession. Open communication with your team about the company’s situation can enlist their support and ideas for weathering the storm. Often, employees appreciate honesty and may contribute cost-saving or efficiency ideas from the front lines. If possible, try to avoid drastic layoffs – not only for humane reasons, but also because when things pick up again, you’ll need trained staff ready to go. Many small firms choose alternatives like reduced hours, temporary pay cuts, or job role flexibilities to share the burden, rather than lose good people entirely. Of course, sometimes layoffs are unavoidable. But consider the long-term costs of losing talent and the short-term hit to morale. On the flip side, if you’re in a position to hire or upgrade your team, a recession can be an opportunity (as mentioned earlier) to attract talent that may be looking for work. Finally, encourage a mindset of frugality and innovation in your team – the goal is to do more with less. Perhaps there are processes that can be streamlined, or creative low-budget marketing tactics (like increased social media engagement, partnerships with other local businesses, etc.) that employees can spearhead. A tight-knit, motivated team, all rowing in the same direction, can be incredibly resilient in a downturn.

6. Leverage Available Support and Resources.

Don’t overlook external help. In most recessions, especially severe ones, there are some government or community programs to aid small businesses – whether it’s emergency loans, tax relief, or advisory services. For example, during COVID-19 the U.S. government offered Paycheck Protection Program loans and other disaster loans that saved many small firms. Stay informed about what’s available: Small Business Administration (SBA) programs, local chamber of commerce initiatives, or industry association relief efforts. Sometimes even negotiating with your landlord or suppliers for temporary relief (like deferred rent or extended payment terms) can provide crucial breathing room. Remember, in a widespread recession, is aware of the situation – you may find stakeholders are more flexible and willing to work with you than you’d expect, because it’s in their interest that you survive too. Pride shouldn’t stop you from seeking help if it can make the difference between closing and persevering.

By implementing these strategies – staying informed, strengthening finances, planning ahead, remaining agile, caring for your team, and tapping into support – you put your business in the best possible position to handle a downturn. You won’t eliminate the pain of a recession, but you can certainly mitigate it and perhaps even find ways to capitalize on it. Think of it like sailing: you can’t control when the storm comes, but you can reinforce your boat, map your course, and skillfully adjust your sails to make it through.

Looking Ahead with Resilience

Recessions, as challenging as they are, have visited us many times before. They are part of the economic ebb and flow, and each one eventually gives way to recovery. As we’ve seen, the history of 20th- and 21st-century recessions is rich with lessons: we’ve learned how excesses build and bust, how policy mistakes or breakthroughs can worsen or lessen the blow, and how resilience and innovation can sprout from adversity. For small business owners and startup founders, these lessons aren’t just interesting stories – they are practical knowledge to apply in your strategy and mindset.

A key theme throughout is balance. Balance between caution and courage, between cutting costs to survive and investing to thrive. History encourages us to be prudent in good times (save for that rainy day, avoid reckless risks) and optimistic in bad times (knowing that downturns spur change and eventually end). If you can internalize both sides of that coin, you’ll make more rational decisions and avoid being swept up in either the euphoria of a boom or the despair of a bust.

Equally important is the human aspect – recessions are not just abstract GDP charts; they affect real people: employees, customers, families. As a business leader, showing empathy, integrity, and steadiness during tough times can set you apart. The trust and goodwill you build will outlast the recession itself. Companies that treated stakeholders right in crises often earn stronger reputations that fuel their long-term success.

No one enjoys an economic downturn. But there is power in preparedness and knowledge. By understanding the early signs of trouble, you can avoid being blindsided. By studying past recessions, you can anticipate how a new one might unfold and impact your market. And by planning and building a resilient business, you can face the future with confidence instead of fear.

In the words of one entrepreneur who steered his small company through multiple recessions: Recessions will come and go. With the insights of history and a strategic, level-headed approach, your business can navigate the storm and even find opportunity in the challenge. The economic seas may get rough at times, but remember – after the storm, the waters calm and the next voyage begins anew, often with those who endured emerging smarter and stronger than before. Here’s to learning from yesterday, thriving today, and confidently anticipating tomorrow’s opportunities, come rain or shine.

Sources:

U.S. recessions timeline and causes

Yield curve inversion as a recession predictor

Post-WWII recessions frequency and duration

1970s oil shock and Fed rate hikes context

Global synchronization of recessions (IMF data)

Impact of Great Depression globally (trade collapse)

Small businesses’ vulnerability in recessions

Small business resilience and market share gains

Companies founded during recessions (historical examples)

Preparatory strategies for businesses (expert recommendations)

Make Your Business Online By The Best No—Code & No—Plugin Solution In The Market.

30 Day Money-Back Guarantee

Create Your E-commerce Store Start now — it's freeSay goodbye to your low online sales rate!